Fees Sorted Well in 2024

Lower-fee funds were likelier to beat their index while higher-fee were more prone to lag or die.

It’s one year not a decade or longer. I get that. However, I still find it instructive to take a look back at the just-finished calendar year to see how active funds have fared.

While success rates tend to be pretty stable (in a not good way) over longer periods, they can fluctuate over shorter periods based on different factors like market direction (up vs down), style leadership, as well as the composition of active funds themselves (if they’re more heavily represented in a style that was friendlier to active than success rates will tick up and vice versa). So that’s why I tally them up.

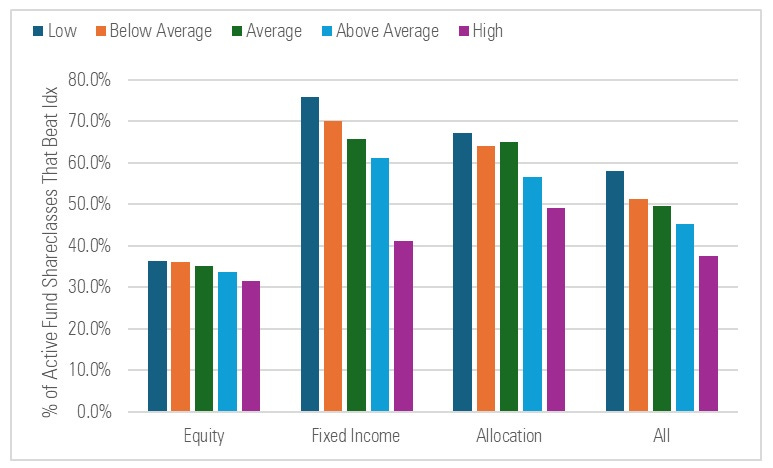

I’ve already shared some data but I was interested to see how active funds did when you sorted them by broad asset class and fee. Did fees do a good job of forecasting which actives would swim and which would sink last year?

Short answer: Yes.

(“Low” are the cheapest funds and “High” the costliest within their Morningstar peer group.)

As is evident from the chart’s left-to-right downward slope, cheaper funds fared better than pricey offerings. They beat their index more often expensive funds and died less often. This was more apparent among fixed income and allocation funds—which tend to be more homogeneous—than equity funds.

The thing about fees is — they’re not something that will give you a big leg up over shorter intervals. Rather, they gradually compound to your benefit, meaning if we were to elongate the study above to span multiple years, you’d see those clumps of bars bend even more steeply down and to the right.

But for 2024 at least if you favored fees, it tended to work in your favor, as you were more likely to have come out ahead of the index you were tracking, equity aside.

fwiw.

The views and opinions expressed in this blog post are those of Jeffrey Ptak and do not necessarily reflect those of Morningstar Research Services or its affiliates.